By Julian Smith | Chief Process Officer

Access to microcredit is often highlighted as a key tool in alleviating poverty. Yet other services often considered complimentary, such as micro-savings, micro-insurance and trainings, are sometimes in themselves a critical service for users.

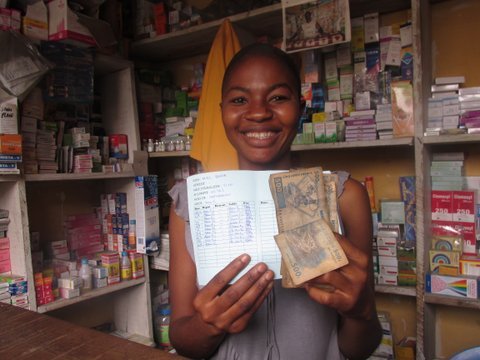

Take, for instance, Pro-Microfinance DR Congo’s ‘Bwakisa Carte’ program, or “savings by card” program. Costing roughly .50 USD for users, members are visited daily by a Pro-Microfinance agents and asked to deposit an amount of their choice with Pro-Microfinance. The agent keeps the deposit of the member in an account for them. At the end of the month, participants can withdraw their savings or continue with another round. Based on a savings model indigenous to the region, the program appeals to busy vendors who deal with small amounts of cash on a daily basis- and for whom a little bit saved is a little bit earned.

Pro-Microfinance USA’s chief process officer Julia Smith visited over two dozen Bwakisa Carte members on September 11, 2014. Members were asked how long they participated in the program, why they participated in the program, and what could be done to improve the program.

Mama Dokas, for instance, is a salted and dried fish vendor originally from Bukavu, South Kivu. With the support of her husband, she started buying her merchandise before becoming a member of the Bwakisa Carte programe in 2013. She’s waiting to save more in order to be able to open a regular savings account with Pro-Microfinance, which will give her access to higher amounts of credit. She hasn’t applied for any microloan yet, but appreciates that the Pro-Microfinance staff are reliable in their collection- meaning she doesn’t have to take time off her long work schedule to also visit her bank.

Mama Tibisa, on the other end of the market, helps her older sister manage a Malewa, or a small food vending stand. She also hasn’t yet taken a microloan from Pro-Microfinance, but just being a part of the Bwakisa Carte program helps her save towards paying for larger costs, such as her children’s school fees and rent. Mam Kisungu, a mother of three and a vendor of raw beans, says she joined the program because she realized that if she saved her money, she could purchase larger sacks of beans. She also appreciates that having savings helps her to be capable of solving problems that might arise, instead of depending on others.

Mama Joline, Antoine, and Astrid are three bean sellers who work together and are all members of the Bwakisa Carte. Mama Joline echos Mama Tibisa, saying “It’s helpful to avoid spending money during the day. When we keep it, in such small amounts it’s not useful. But when we save it, its enough to cover bigger expenses, like our monthly rent”.

Members of the Bwakisa Carte program are also eligible to apply for PMI’s credit products and receive microloans of up to 300 USD. But for many of the clients visited, being able to manage their savings is a first, and last, step in meeting cash-flow shortages.

When savings alone can enable vendors to reinvest in their stock and cover household expenses, the act of collecting savings for members becomes a key tool itself in managing and overcoming the challenges of being a small-scale vendor in DRC.

By Kym Park | Chief Communication Officer

By John Kavyavu and Julia Smith | CEO

Project reports on GlobalGiving are posted directly to globalgiving.org by Project Leaders as they are completed, generally every 3-4 months. To protect the integrity of these documents, GlobalGiving does not alter them; therefore you may find some language or formatting issues.

If you donate to this project or have donated to this project, you can receive an email when this project posts a report. You can also subscribe for reports without donating.